Let's take the data from previous steps

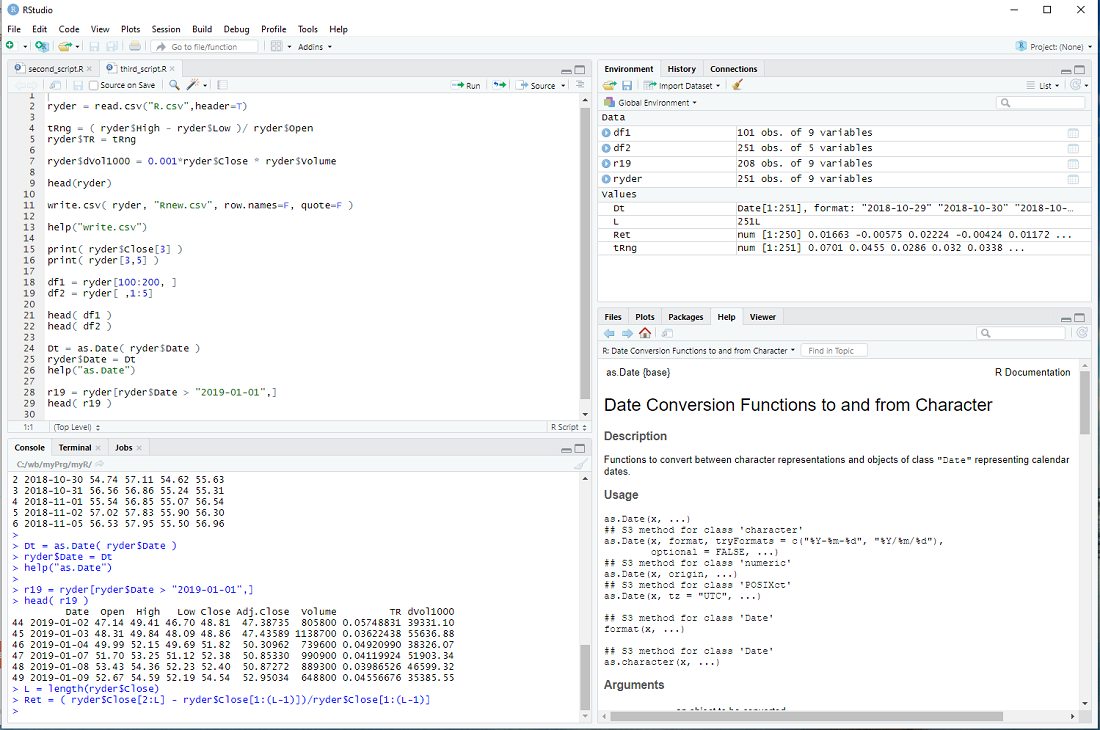

ryder = read.csv("R.csv",header=T)

and calculate the "trading range", normalized by the open, for every day

tRng = ( ryder$High - ryder$Low )/ ryder$Open

This generates the vector tRng , calculates the difference of high and low for every day, divided by the open and assigns the result to the elements of tRng, i.e. 251 * 2 calculations, all in one line.

We can now add this vector to the data frame ryder

ryder$TR = tRng

Now let's calculate the dollar trading volume in thousands for each day and add it as a column

ryder$dVol1000 = 0.001*ryder$Close * ryder$Volume

We can take a look at the first entries of the data frame with the head() procedure

head(ryder)

but we would see the same thing in window 3 top right.

If we want to store the expanded data frame in a file, we could do it as follows

write.csv( ryder, "Rnew.csv", row.names=F, quote=F )

I set the parameters so that it has the exact same format as R.csv.

You can get help with

help("write.csv")

The columns of ryder are: Date, Open, High, Low, Close, Adj.Close, Volume, ...

and we can access each column by its name

print( ryder$Close[3] )

But we can also access the elements of a data frame directly

print( ryder[3,5] )

The first index is the row and the second the column (Close is the 5-th column of ryder).

We can also slice data frames

df1 = ryder[100:200, ]

head( df1 )

Notice that the blank entry, instead of an index, means all columns.

df2 = ryder[ , 1:5]

head( df2 )

The blank entry, instead of an index, means all rows.

Until now, I have not mentioned the column Date and for a good reason - it is a bit of a mess.

The read.csv procedure interprets it as a Factor and not a date, although the entries are formatted so that R can interpret it as date.

But we can fix that

Dt = as.Date( ryder$Date )

ryder$Date = Dt

help("as.Date")

The as. family of conversion functions is quite useful in R.

This allows us to slice the data frame ryder in yet another way ...

r19 = ryder[ryder$Date > "2019-01-01",]

head( r19 )

... and concludes this step of my introduction.

exercise: Calculate the returns of ryder for each day, beginning with the 2nd day.

The return on the 2nd day is ( ryder$Close[2] - ryder$Close[1] )/ryder$Close[1] ,

the return on the 3rd day is ( ryder$Close[3] - ryder$Close[2] )/ryder$Close[2] ,

etc. Now calculate it in one line and assign the results to a vector Ret.

hint: Use L = length(ryder$Close) in your calculation ...